The Slings and Arrows of Outrageous Fortune

A look at what normal variability in trading results can really mean.

[dc]T[/dc]raders and investors are often unprepared for the variability of their trading results. This is difficult on many fronts. First, and most obviously, perhaps you won't make as much money as you "should" from trading your system, or maybe you will make a lot more. Maybe your system will seem to stop working for a time. (And if so, how will you separate "for a time" from a more serious permanent breakdown in the methodology?) This variability can also make evaluation your results very difficult, and can hide the truth of your and your systems performance. Consider the following trading system.

- Risks a fixed amount R per trade. For the purposes of this discussion, R = $2,000.

- Losses are always exactly -1.0R and wins are always +1.2R.

- The system wins 50% of the time, loses 50% of the time, and has no breakeven trades.

- The expectancy of this system is positive, and is 0.1. (Win percentage * Average win) – (Loss percentage * Average loss) = 1.2 * 0.5 – 1.0 * 0.5 = 0.1.

- This means that for every dollar risked, on average, we receive that dollar back, plus another $0.10. Over a finite time span, results can be much more variable than this would suggest.

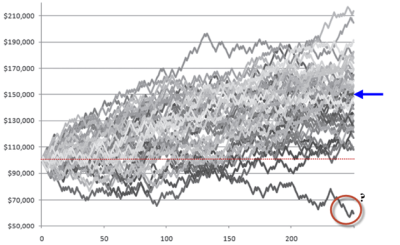

Now, assume that you have to trade the system and assume that you will trade it for 250 consecutive trades with a $100,000 starting account, risking $2,000 per trade. What results do you expect? On average you "should" end up with a total account value of $150,000 at the end of 250 trades, but how sure are you? Could you lose money trading this positive expectancy system?

Take a look at the following chart, which shows the results of 100 traders trading 250 trades of the exact same system. (A useful way to think about this is to think that these traders were maybe working in parallel alternate universes. Each run is completely independent of the others.) No trader made any mistakes or errors. The only difference was the random distribution of wins and losses, with a 50% probability on each individual trade. The blue arrow shows the expected value of the system, and we see that many of the traders ended up in that neighborhood, but results, as they say, vary. Some traders doubled their money, and one, out of this sample of 100, very consistently lost money even though he made no mistakes and was trading a positive expectancy system. That is a critical point--no one made any mistakes here. No one held a loser past its stop point, no one got emotional and took "bad trades", and no one made any execution errors. The variability in these results is all due to normal statistical fluctuation--the slings and arrows of outrageous fortune, as the Bard said--and your own trading (and backtesting) will be subject to the same laws of nature. We'll explore this in more depth in future blog posts, but, for now, spend some time trying to consider the performance of the top and bottom group of traders, the different impressions they might have had of the system and of their own performance.