Are you losing when you should be winning? Here's something you might be missing.

Most people think about where to get into and out of positions. Most traders know how important it is to follow their rules, and most traders are always working toward being more disciplined. These are important pieces of a successful investment strategy, and most traders work on these things. But there's one thing that is usually neglected, and it can make winners into losers. When you trade, how much do you trade? How big are your positions?

This question of how much to trade--position sizing--is critical. Trade too small, and no matter what you do, you won't make enough money to justify your time spent trading. Trade too big, and you risk losing everything.

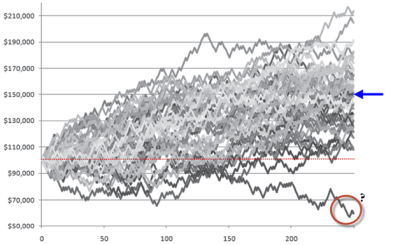

I am in the process of creating the next module of my free trading course, and it will focus on this question of how to size positions appropriately. I created an example, a long time ago, of a simple positive expectancy system (the system wins 50% of the time and wins are 1.2X the size of losses. More details of the system are here) and then created a simulation where many traders would trade the system for 250 trades. Starting with $100,000 and risking $2,000, here are the results of 50 random traders trading the system:

I've used this example before, and even put it in my first book. The point here, is that results can be a lot more variable than you'd think. None of these traders made mistakes, and there were no surprises--over 250 trades (a large sample) of this positive expectancy system, one unlucky trader lost money, and quite a few struggled. There are lessons here that should give us pause for thought, but let's focus on something a little different. What happens if we risk different amounts on each trade?

A few points to notice: the more you risk (per trade), the more you make (on average), but there's a huge red flag--at higher risk levels, the chance of something very bad happening becomes extreme. Remember, this was the same positive expectancy system (expectancy was +0.1) with the same set of trades for each column; the only thing that changed was how much we risked on each trade. At $8,000 risk per trade, 11% of the accounts went bankrupt--trading a winning system! At $25,000 risk, nearly half the accounts went bankrupt. These risk levels seem crazy(or, I hope they seem extreme to you), but many traders are working with risks like this, whether they know it or not.

A picture is worth a lot of words; here's an illustration of the equity curves from the table above. Pay special attention to the number of traders who "crater" into the zero line--one bankrupt, they are out of the game and have to stop trading.

Most people are inclined to focus on the good things that could possibly happen, even if they are not likely--this is why lotteries and casinos exist. Use too much risk, focus only on the upside, dream of the big home runs, and you're rolling the dice; your entire trading account becomes a lottery ticket. Focus on the risk first, manage that risk, and make sure that each of your trades is a correct, consistent bet size, and you're on the path to being a professional trader and working toward consistency.

A few final thoughts: these examples focus on risking a specific dollar amount per trade. That's ok, and it's better than no plan at all, but risking a fixed percentage of your equity (fixed fractional risk) probably makes more sense; as your account grows, you will automatically risk larger dollar amounts and everything scales proportionally. The question of how much to risk does not have an easy answer. There are optimized approaches like the famous Kelly criterion and Ralph Vince's optimal f, but these can be quite aggressive and may have unacceptable drawdowns for many investors.

A reasonable compromise is to choose a risk per trade of somewhere between 1% - 4% of your equity. Again, the right answer depends on your psychology, trading objectives, and characteristics of your trading method, but this is a good rule of thumb. Paying attention to this critical piece of your investment strategy can make the difference between failure and success.