Much of my published work focuses heavily on technical analysis. I’ll discuss the reasons behind this decision more in the future, but I have also considered fundamental, macro, and economic factors in my analysis for over a decade. Today, I want to share a few thoughts on GDP, one of the most important of the headline economic numbers.

For some of you (with business school backgrounds) this will be review and elementary, but I still hope to show you a few tweaks that can change the way you look at the number. For some of you, especially those of you who come from a purely technical background, much of what I write here will be completely new.

One last word before I begin: I’m slightly oversimplifying many aspects of this post. There is plenty of debate about what GDP means, several different ways to measure it, and the whole discussion is often tinged with politics. If you disagree with what I write here, you’re probably on solid ground to do so, so no worries!

What is GDP?

GDP is basically the total value of all goods and services produced by a country. That’s it: it’s a simple concept, and it’s obviously important.

But measuring it is almost hopelessly complicated. Who would think we could calculate the value of every widget or service produced in an entire country? (And then to do the same thing four times a year!) In practice, the actual GDP number includes a lot of statistical guesswork and processing, and the number is subject to constant revision.

GDP is reported, in the US, near the end of the month. The first month of the quarter gives the first estimate for the previous quarter, and that estimate is revised on the following two months. It stands to reason that, barring some major revision, the first estimate of the quarter (which we’ve just seen) is the one most closely watched. As for where to get the data, best to go straight to the horse’s mouth and get the raw data directly from the Bureau of Economic Analysis.

GDP Components

One common way to calculate GDP is to consider it the sum of:

- Consumption: How much money people spent on things like food, rent, gasoline, luxury goods, medical services, etc.

- Investment: Business investment (building a new plant, buying a new machine, etc.) and housing is counted here.

- Government spending: The military is a big component here, but this also counts government salaries.

- Net exports: For the US, this number is usually negative (i.e., Net Imports), which we might argue is what a wealthy nation could reasonably be expected to carry. Since we’re measuring what a country produces exports must be added to the number.

- Inventories: Properly included in investments (the accounting assumption is that something produced but unsold is bought by the producer), but important because we are counting the value of what is produced, not just what is sold.

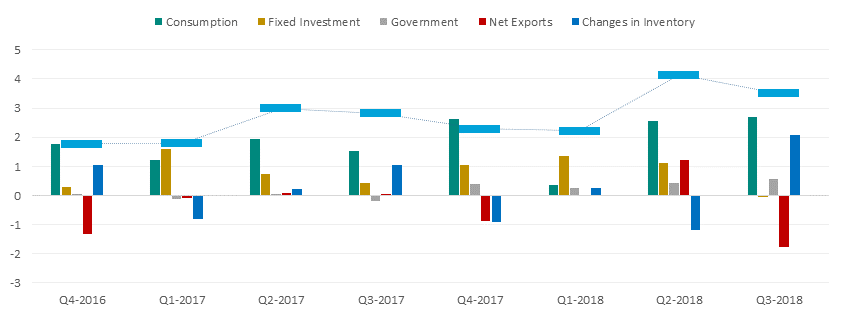

Look at the chart below, which shows how each of these components played into recent GDP numbers.

What do we see today? Again, this is open to interpretation, but here are a few points to consider:

- Consumption is strong. This is a good measure of the real strength of the economy. People buy things because they are confident. One of the concerns we had through much of 2016-2017 was the relative absence of Consumer buying, and this is a resounding strength in Q2 2018 and Q3 2018 numbers.

- Fixed investment is very low in the recent report. While this was largely expected (because housing numbers have been soft) we also know that housing tends to be a prescient indicator for the economy. (We’d also need to dig into durable goods, auto sales, etc., which are buried in consumption.)

- Government spending is a relatively small, but relatively constant contributor.

- Exports… um… ouch. Net imports were a major contributor to Q2, and this has been reversed into a frankly stunning draw on exports for this quarter. We are still trying to understand the impact of tariff and trade war discussions, but this measure at least calls some of Q2’s optimism into question.

- There’s a huge inventory build. It’s hard to know quite what to think of this one, as there may be more trade-related impacts lurking here (i.e., manufacturers rushing production ahead of price hikes on raw materials). Strength of manufacturing sector is also a closely watched measure, and you don’t build inventories like this without some considerable strength, but is it sustainable? If we’re looking at an individual company, an unexplained explosion in inventory is potentially bad (inefficient use of capital? People just aren’t buying your stuff anymore?). Do the same concepts apply at the national level?

These are the kinds of questions we need to ask about a GDP release. Some of those questions will be clarified in the next few weeks, and some will probably remain for a while. Regardless, it’s good to think beyond the headline, and beyond a simple “GDP beat or miss” and to dig a little bit deeper into the data.

If you’d like to see more of my work that uses macro and fundamental elements, I’d like to invite you to check out the research I write for Talon Advisors. Every weekend, we publish a substantial report covering action in global stocks, currencies, and commodities, with an emphasis on future market direction, risk management, and the contribution of fundamental/behavioral factors. We also publish a shorter daily note and an extensive quarterly piece that does a deep dive into macroeconomic data, relationships between global economies, seasonality, the impact of volatility, and much more. Because much of this analysis is high-level, we also publish a set of example trades that boil these perspectives down into actionable ideas. You can see the performance of this set of trades here.

For a limited time, you can use code pumpkin15 for a 15% lifetime discount for your subscription (for individual traders/investors). Click the button below and sign up today.

[button link=”https://www.talonadvisors.com/users/sign_up” newwindow=”yes”] Sign up today![/button]