[dc]A[/dc]ttention is a precious resource. None of us, whether individuals or institutions, have an unlimited supply of attention. Part of the process of trading successfully is figuring out where to focus that limited attention. Part of this is dynamic; as trades develop we are able to spend different amounts of time and attention on potential new entries, exiting trades at a loss, taking partial profits, looking for secondary entries, and all the other tasks of trade management. Of course, unexpected events can change things dramatically, and this is one of the challenges of our discipline. Today, though, I want to share a few ideas on something a bit more routine, and share some of the ideas I’ve found useful for stock traders looking to find the best trading candidates.

There are roughly 7,000 – 8,000 listed stocks on US exchanges–a universe that is far too large for any one trader to successfully navigate. Most traders think right away about screening candidates, but there’s an important first step: what would ideal candidates for your trading style look like? Most people never ask that question, starting, instead, with some volume, liquidity and activity cutoffs. (Those cutoffs make sense, but I think they are a good second step. As usual, thinking and asking the right questions is the first step!) For instance, active daytraders need enough “play” within each trading day to make profits. For a trader like this, getting into a position in a stock that “doesn’t move” is a waste of time, so these traders might naturally filter for average daily range (the average distance between the high and the low of the day). However, if you are a swing trader, maybe you don’t care about average daily range–what if, hypothetically, you could identify a stock that went up $0.25 every day but only had an average range of $0.05, intraday? (You can’t, but this is an extreme example as a thought experiment.) That stock would be death for a daytrader, but might be an ideal candidate for a swing trader looking to hold for short swings. So, first, understand what you hope to accomplish with the screens for your trading style.

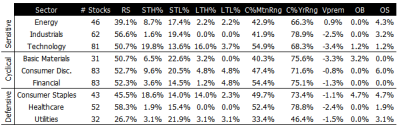

Filtering for liquidity

For most traders, I would suggest that volume and liquidity should, in fact, be near the top of the list of concerns. Trading a very inactive $50.00 stock with a $0.25 spread is difficult, and you should always consider the conditions you might face if you need to get out of that position in a hurry. Could you be slipped $0.10? $0.50? More? Yes, it can happen with any stock, but it’s much more likely to happen with a thin stock. Where are the “right” cutoffs? The answer, again, depends on your style, but I think we can set rough guidelines at perhaps at 1MM shares a day for active traders, and maybe 500,000 shares / day for position traders. Again, it depends on many things. Even an active stock can be pretty thin at, say, 1:00 PM on a summer Thursday, so there is an element of skill and ongoing adaptation needed, but these broad volume levels are a good start.

The combination of trading size and frequency matters, too. If you are a daytrader trading a few thousand shares, with some patience you can navigate most stocks. If you are a larger trader and need to put on positions that are, say, hundreds of thousands of shares, that takes time. Dollar volume (average daily volume * average price, over the same window) is another potentially useful measure; when you standardize for price, it becomes immediately obvious that 1MM shares average volume on a $10 stock is different from those 1MM done on a $100 stock. Average daily dollar volume might be a useful measure to consider, as well.

The combination of trading size and frequency matters, too. If you are a daytrader trading a few thousand shares, with some patience you can navigate most stocks. If you are a larger trader and need to put on positions that are, say, hundreds of thousands of shares, that takes time. Dollar volume (average daily volume * average price, over the same window) is another potentially useful measure; when you standardize for price, it becomes immediately obvious that 1MM shares average volume on a $10 stock is different from those 1MM done on a $100 stock. Average daily dollar volume might be a useful measure to consider, as well.

Filtering for volatility

We already touched on this, but some traders may wish to filter for stocks that have a certain average daily range. An extension of this is that it is also possible to remove “flatline” stocks. For instance, if a stock, in its recent history, shows very little price change, this is sometimes characteristic of “deal stocks” or stocks where something else is going on. Remove these or leave these in your universe, as you see fit. (I tend to leave them in because I want to see them, but you have to be aware.)

Options traders may also wish to filter for various aspects of volatility. Possible measures are ratios of shorter to longer term historical volatility, of longer to shorter term implied volatility, or of implied volatility to historical volatility. Be careful, because some of the “first level” options trading material sold to retail traders makes very dangerous simplifying assumptions; for instance, we might be told to look to sell options in stocks which had very high implied volatility relative to historical (realized) volatility. The options market is smart, and those options are often expensive for a reason. There is no free lunch. Furthermore, realize that any implied volatility number you see has many calculations “baked into” it, and there will sometimes be distortions. You can navigate these on an individual stock with no problem, but what if you are doing a scan on hundreds of names? Then, these distortions will not be caught and may be more of a problem.

While we’re on the topic, if you’re looking to trade options, it probably makes sense to filter the universe for optionable stocks as a first step and then perhaps to look for certain liquidity levels on the options.

This is a good place to stop for today, I’ll finish up with part 2 of this post tomorrow, and dig into a few more things we should consider.