I thought it would be interesting to update this post, which was a fairly in-depth look at trading some pullbacks in copper. If you haven’t read it, go read it first, and if you read it a while ago maybe glance at it again so that what follows will make more sense. Today’s lessons are important: indicator divergence, entry on volatility contraction, and trade management.

Momentum divergence

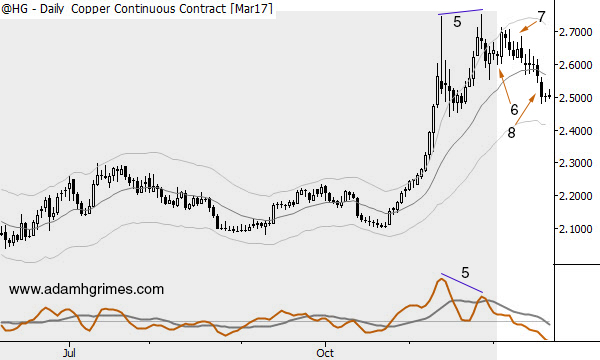

I’ve lightly shaded the part of the chart covered in the previous post so we can see what’s new, and I also picked up with the label 5 since I finished that post with 4. At 5, we see a pretty glaring example of a momentum divergence on the MACD. For those who aren’t familiar with the concept, we assume that the fast line (orange line) of the MACD measures momentum, and if we see a new price high made on lower momentum (i.e., a lower reading on the MACD), then we say we have a “momentum divergence”.

One of the great things about coaching and mentoring smart traders is that they ask hard questions! Several of my students asked me this week about divergence, so I spent a few hours discussing and thinking about it. To my thinking, this is a grey area in technical analysis. Most of my readers know that I’ve been a bit obsessive about testing technical concepts with statistical tools. Some things do work (good examples are pullbacks and some types of overbought/oversold readings.) Some tools very clearly don’t show any edge (moving average crosses or touches, and the famous Fibonacci levels). But some things fall in a big grey area.

Any tool that has a subjective component is difficult to test statistically, and we should be highly suspicious of those tests. I’ve tested divergences a few ways: I’ve done some statistical work looking at strength and magnitude of extension following pullbacks, qualifying those swings by presence/absence of momentum divergence. In that test, I found no difference. I also did a relatively small set (a little over a thousand) of “by hand” backtesting of setups with and without divergence, and could see no difference between the two sets. So, at least in my own trading, I don’t use or look at momentum divergence, but there’s more to the story.

Measuring might be the problem

Certainly, there is validity to the underlying concept: if a market makes a new high on strong momentum and then pulls back, we are likely to have at least another attempt to go higher and maybe a whole new leg. On the other hand, if the market makes that new high with a weak move, we’re probably less likely to see a new leg up. This is, least to my thinking, almost certainly a valid concept, but adding an indicator to measure and structure it results in us doing a joint test of both the underlying (probably valid) market concept and the specific structure of the indicator measurement.

It’s this joint test that seems to fail, but this leaves us with a few problems: for developing traders, it really is helpful to have some firm rules and measurements. For any systematic use, we must have clear and consistent rules. I’ll almost never look at an indicator divergence, but I certainly respect the concept. Because of this, I was not even considering buying the pullback at the point marked 6 on the chart, though the small bars near the top of the most recent flag might well provide a good entry point.

Trade management matters… a lot

Your results are the outcome of all your trading decisions, and exit decisions are as important as entry decisions. Though I have no interesting in buying after (6), consider where and how you might have managed a long trade there: initial stop placement should probably be in the 2.45 – 2.53 range, and this can be tightened aggressively after the big up bar following (6). This bar is strong confirmation of the trade, and is followed by an inside bar near the high of that bar—so far, everything looks good for a long trade, but the situation changes at (7).

At (7) we start to see enough sideways/downward action that the long trade is no longer working as expected. Context matters—if the setup for the pullback had been stronger, we might hold through the garbage at (7). Given the questionable context (multiple climactic overextensions setting up the pullback, some form of momentum divergence, and the 6+ year downtrend copper has been in, we might look to limit risk more aggressively and be out of the trade with a small loss. Small losses, if taken for the right reasons, are good losses.

Shades of grey

This type of discretionary chartreading does not live in a black and white/right and wrong world—everything is shades of grey. For the reasons I’ve argued above, I had no interest in a long entry around (6), but you might reasonably have disagreed. You might also choose different stops and trade management techniques, but all of this rests on the ability to take each new piece of information (bar) and use it to better understand the developing story of the chart.

Speaking of which, we get a strong downthrust at (8) that suggests a mini-climax on a lower timeframe, but may shift the balance even more away from the bulls. Given that context, the last, small bars on this chart might provide a reasonable spot for a short entry on further weakness, though then we need to turn some attention to the developing bull flag on the weekly/monthly timeframe.

Putting it all together

This series of posts has been a bit more conflicted than most, but I wanted to show you one way to look at charts in dynamic markets. Answers are muddy and confusing, and we can always look back and see something we should have missed. The “game” of trading is to make the best decisions you can, with absolutely conviction, given the information you have at the time. However, we also have to know that information is always incomplete, and what we did with full conviction today may need to be reversed tomorrow—not always easy to do, but essential for your success as a discretionary, technical trader.

Thanks for the great and informative post Adam. Question regarding the MACD – if you don’t look at it for momentum divergence, why do you have it on your charts? Does it serve another purpose?

Thanks a lot, those discussions are very helpful and interesting.

I was also thinking quite a lot about momentum divergence in the recent past… I also did not take the trade, but more for PF reasons.

When I looked at the momentum divergence I was thinking of how far the price would have to go up to NOT make a momentum divergence – the close of the 2nd peak would need to be around 2.85 or higher, i.e. there would be easily a handful of free bars with decent size above the upper K-Channel which then would point to a potential climax and an absolute no-go to enter long for me. In other words, I think it is nearly impossible not to get a momentum divergence at point 5. I was not very succesful in testing MACD highs in my own work, so I put it back into the shelf to re-visit some time in the future.

In summary, I’d say if I’d sense a huge buying/selling pressure imbalance reflected by clear and strong MACD high, I would not wait to see a second and even higher re-confirmation of the same concept.

Thank you for this article Adam. Your perspective on momentum divergence is very interesting. Now, I’m just starting out and aim to learn more about your approach toward Technical Analysis as a way to cut out some of the information noise that is plaguing my mind. I really like it so far, it is something like a “TA Zen”. Clean, simple, efficient.

But I’d like to share one classic TA concept that I have successfully used in the past which might be something to explore (as a hypothesis to set up the momentum divergence experiment more cleanly – although it imho still depends a lot on indicator configuration). It states that: “Momentum trend leads price trend”. This is essentially a generalization of the rationale you outlined in the article above just with the added spin to view momentum as a trending indicator – which opens the possibility to apply the standard trend analysis repertoire to the preferred momentum indicator.

Divergence is then just a state, i.e., the situation where momentum and price trend are not aligned and could be used as a filter (just like you suggest) or as a signal on it’s own (although price action imho always takes precedence). A break of the momentum trend indicates continuation and so on and so forth.