Reader question: is VWAP useful?

I received a good question from Brent:

I recently watched [a presentation someone else did] about VWAP and they seemed really convinced it was an effective indicator. I am curious if you have studied VWAP in recent years? Their contention is the black boxes key around VWAP which makes it very useful. I know you said you could not find an edge with volume, but was curious if you have examined this since all the program trading has ramped up...

Well, the short answer is yes I've looked at it, and no I haven't found an edge. But I think that answer deserves a little more qualification and explanation.

First, let me explain my thinking in testing moving averages. Basically what I'm looking for when testing any level is some evidence (or even suggestion) that price movement is somehow "non random" following price engaging the moving average. You could start, for instance, with recording all times price touches a moving average, looking at returns following those points and comparing it to all market action. Of course, we need to make some decisions; price coming into a moving average from above is probably different than price coming from below, a moving average breaking might be different than it holding, etc. We soon realize that this isn't quite as black and white as it might seem, because then we ask things like "is it different if price comes to the moving average from far away or if it slowly 'edges' into the average? What if the market is trending?"

The questions can go on, and each time we cut the data a different way we are degrading the test a little bit. In most of my work, I've tried to stick to higher level questions and simply looked for some evidence that there is something interesting happening around moving averages. I cannot find that evidence, nor can I find it in any calculated level like Fibonaccis.

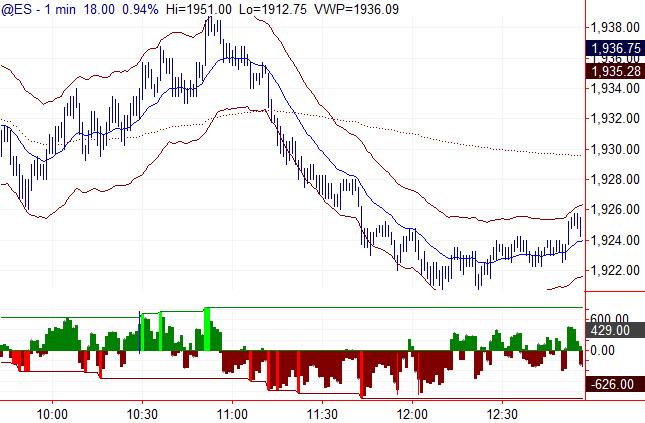

When I've looked at VWAP on different timeframes, I find it's no different than any other average, which is to say that price action following price engagement the moving average is random and unpredictable. Someone selling you something based on VWAP is going to give you many arguments why it should work or why it should be so, but ask them for statistical evidence. We always hear why a level should work (or how it reflects the structure of the Universe or something else), but the people selling these things, oddly enough, never seem to have done the work to show whether it is true or not. Don't be dazzled by marketing pitches for technical concepts.

Considering further, I find I don't need these levels to trade well, and I also know that humans are susceptible to a number of cognitive biases that might make lines on a chart look important when they are simply random. So, my personal answer, based on deep quantitative work and my trading style, is that I think these levels are meaningless and that people using them are deceiving themselves. I ignore them and ignore any commentary based on them.

Is that the last word on the subject? Of course not. Anecdotally, I know many traders that use VWAP, but I also know many that use moon cycles or calculations based off the Jewish calendar. Me? I'm a cranky nihilist and something has to meet a pretty severe standard of proof before I'll use it, but that's just my answer. The rest of your question (which I edited) suggests that you're on track to do these tests yourself, and I think that's where most people find answers. As one of my mentors used to say, when you have a question, ask the data. Ask the data.